GST has rolled out and paved the way for a uniform and systematic reporting system that is seldom found anywhere else. This transaction-wise, destination-based reporting system provides for a much effective credit flow, removes chances of corruption and illegal transactions.

To achieve this, the government has come up with an effective form-based reporting system that needs to be filed either monthly, quarterly or yearly, as the case may be, by the dealers and manufacturers. The aggregation of information uploaded by all the dealers will lead to a common reservoir of data, which can be accessed by either. Moreover, dealers can view their credit statement or payables with respect to GST easily in a common internet portal.

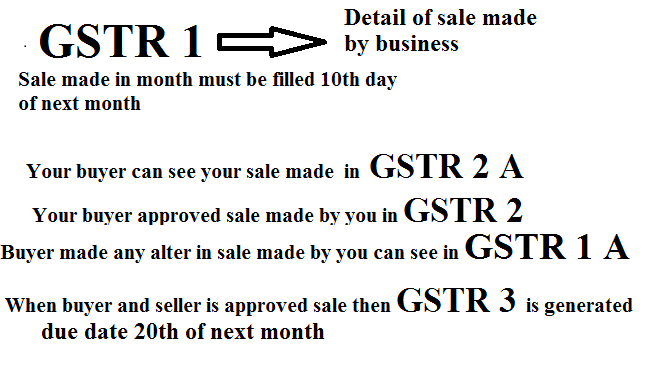

What Is GSTR-1 ?

It all starts with GSTR-1. It is where the suppliers will report their outward supplies during the reporting month. As such, all registered taxable persons are required to file GSTR-1 by the 10th of the following month. It is the first or the starting point for passing input tax credits to the dealers.

Who needs to file GSTR-1?

GSTR-1 has to be filed by “all” taxable registered persons under GST. However, there are certain dealers who are not required to file GSTR-1, instead, are required to file other different GST returns as the case may be. These dealers are E-Commerce Operators, Input Service Distributors, dealers registered under the Composition Scheme, Non-Resident dealers and Tax deductors. It has to be filed even in cases where there is no business conducted during the reporting month.

How to file GSTR-1 In few steps.

What needs to be filled in GSTR-1?

GSTR-1 has 13 different heads that need to be filled in. The major ones are enlisted here:

- GSTIN of the taxable person filing the return – Auto-populated result

- Name of the taxable person – Auto-populated field

- Total Turnover in Last Financial Year – This is a one-time action and has to be filled once. This field will be auto-populated with the closing balance of the last year

- The Period for which the return is being filed – Month & Year is available as a drop down for selection

- Details of Taxable outward supplies made to registered persons – CGST and SGST shall be filled in case of intra-state movement whereas IGST shall be filled only in the case of inter-state movement. Details of exempted sales or sales at nil rate of tax shall also be mentioned here

- Details of Outward Supplies made to end customer, where the value exceeds Rs. 2.5 lakhs – Other than mentioned, all such supplies are optional in nature

- The total of all outward supplies made to end consumers, where the value does not exceed Rs. 2.5 lakhs.

- Details of Debit Notes or Credit Notes

- Amendments to outward supplies of previous periods – Apart from these two, any changes made to a GST invoice has to be mentioned in this section

- Exempted, Nil-Rated and Non-GST Supplies – If nothing was mentioned in the above sections, then complete details of such supplies have to be declared.

- Details of Export Sales made – In addition to the sales figures, HSN codes of the goods supplied have to be mentioned as well.

- Tax Liability arising out of advance receipts

- Tax Paid during the reporting period – it can also include taxes paid for earlier periods.

The form has to be digitally signed in case of a Company or an LLP, whereas in the case of a proprietorship concern, the same can be signed physically.

Common Mistakes while filing GSTR-1

The mistakes can be as puny as mentioning incorrect HSN codes, Service Accounting Codes and can extend up to mentioning incorrect GSTIN, charging incorrect rates of tax, treating a sale as an intra-state sale instead of inter-state sale or vice versa, mentioning a tax invoice twice and the like. The supplier while filing the GSTR-1 can make these common mistakes. Apart from the above, situations may arise that ship to address of the customer can change. This common change can be witnessed while filing GSTR-1.

How to amend GSTR-1?

There may be cases wherein details mentioned by the supplier are incorrect. In these cases, there is a possibility for the dealers to amend the errors or omissions after filing GSTR-1. In a normal scenario, the details filed by the supplier is rejected by the recipient of the goods or services, then the supplier will receive an intimation to that effect, wherein he can amend the same. Where the recipient inadvertently accepts the invoice, oblivious of the error, then the supplier has to report the same to the Jurisdictional Authority citing such error and its rectification. The Jurisdictional Authority will have to option to make good such error, after ascertaining the facts of the case.

Where an inter-state sale is treated as an intra-state sale and subsequently, IGST is charged instead of CGST and SGST, then the supplier has to pay the amount of IGST separately to the Ministry and claim for a refund of the excess CGST or SGST. Again, he also has the option to claim input tax credit on the CGST / SGST amount inadvertently paid by him against CGST, SGST or IGST output liability, as per the prescribed rules.

In some cases, the supplier may be required to change information in a tax invoice, which is already uploaded in GSTR-1. It has to be noted that if the recipient accepts the details of the supplier as mentioned in the GSTR-1, then the supplier will have no option to amend or make any changes whatsoever in the invoice document. The supplier has to issue a supplementary invoice or a credit note against the invoice in which he wants to make any changes.

To negate the effects of the double claim of input tax credits, suppliers shall install a system, which derives a unique combination of financial year, invoice number, and the GSTIN. The system will automatically display the error in case there is a duplicate invoice being punched in.

There can be chances that Point of Supply in an invoice is changed over a reasonable period of time. This new point of supply can happen to be in a different state. In that case, SGST part charged will be reversed and passed on to the new state.

Common Questions Regarding GSTR-1

1) What is the checklist before filing Form GSTR-1?

The first and foremost requirement is having a valid Goods and Services Tax Identification Number (GSTIN). The supplier will be notified with a User ID and Password that will enable the user to file returns. Next, the supplier will be required to have a valid digital signature certificate (DSC). This DSC is obligatory for companies, LLPs (Limited Liability Partnerships) and FLLPs (Foreign Limited Liability Partnerships). Other suppliers, i.e. Proprietors, partnership concerns, HUF, etc. have the option to “E-sign” the form. In that case, a valid Aadhar Card Number is required. An OTP for verification shall be sent across on the registered mobile number as mentioned in the Aadhar Card.

2) How shall I file GSTR-1?

After going through the checklist, suppliers need to log in to the GSTN portal with the given User ID and password, follow these steps to file their returns successfully.

- Search for “Services” and then click on Returns, followed by Returns Dashboard.

- In the dashboard, the dealer has to enter the financial year and the month for which the return needs to be filed. Click on Search after that.

- All returns relating to this period will be displayed on the screen in a tiled manner.

- Dealer has to select the tile containing GSTR-1

- After this, he will have the option either to prepare online or to upload the return.

- The dealer will now Add invoices or upload all invoices directly

- Once the entire form is filled up, the dealer shall then click on Submit and validate the data filled up

- With the data validated, dealer will now click on FILE GSTR-1 and proceed to either E-Sign or digitally sign the form

- Another confirmation pop-up will be displayed on the screen with a yes or no option to file the return.

- Once yes is selected, an Acknowledgement Reference Number (ARN) is generated.

3) What is the due date of filing GSTR-1? What if I don’t file my returns within the due date?

The due date for filing GSTR-1 is 10th of the following month. If the dealer does not file GSTR-1 where it is mandatory to do so, then a late fee will be charged to the dealer.

The late fee is an amount of Rs. 100 / act / day, i.e. Rs. 300 shall be charged on account of IGST, CGST and SGST per day. Moreover, this late fee is calculated automatically after filing of GSTR-1.

Read about penalties under GST.

4) Can you upload invoices any time before filing the return?

Yes. Invoices can be updated on a regular basis before filing GSTR-1. Technically, dealers have a time slot of 40 days to upload their invoices, i.e. from 1st of the reporting month till the 10th of the next month. There can be several changes made to the list of invoices during this period.

5) The field “turnover” is a mandatory field in GSTR-1. How shall I fill it up?

This field is a one-time field and has to be filled up manually during the first return. It will be automatically populated every month based on the details furnished in the return.

How To File GSTR-1 Online?

Apart from filing GSTR-1 directly on GSTN portal, you can use third party softwares which are simpler to use. Most of these software accept data from your existing accounting software and help you upload it to GSTN portal. Almost all the GSPs have come up with their return filing solution.

If you want to avoid multiple steps and hassle of using lot of softwares, try ProfitBooks today. Its an easy to use accounting software with super fast GST return filing. Its designed for business owners who do not have any accounting background.